Michael Vandi

A mortgage pipeline can look full, yet many loans aren’t actually advancing. Files wait on a missing bank statement, a condition remains unresolved, or underwriting takes longer than expected.

When delays stack up, approvals drag out, and deals become harder to close. Lenders who keep their pipeline organized see more consistent closings and fewer issues.

This article explains how mortgage pipeline management works, where loans tend to get stuck, and how to keep them on track through closing.

TL;DR

Mortgage pipeline management helps lenders track loan progress and spot issues so approvals don't get delayed.

Missing documents, underwriting queues, and compliance errors often slow down loan approvals.

Tracking metrics like fallout rate and processing time helps lenders understand pipeline performance.

Setting clear requirements and grouping similar loans keeps reviews more consistent.

Addy AI helps review files, flag missing documents, and follow up with borrowers automatically.

What Is a Mortgage Pipeline?

A mortgage pipeline is the list of loans a lender or broker is handling from the moment a borrower locks a rate until the loan closes or is sold. It shows which files are waiting on documents, being reviewed, or underwritten.

Lenders, mortgage bankers, and brokers use pipeline management to track approvals, spot issues early, and keep loans progressing through each stage. It helps assign work so underwriters and processors don’t get overloaded when application volume increases.

Pipeline management ties into mortgage pipeline hedging, which helps lenders deal with interest rate changes while loans are still pending.

Knowing where each loan stands and what it needs next helps prevent delays and keeps the process consistent from application to closing.

Key Metrics for Mortgage Pipeline Optimization

You need the right data to understand what’s happening inside your mortgage pipeline. Without them, it’s hard to tell why a loan didn’t close or why approvals take longer than expected.

Here are the key metrics to watch:

Pull-through rate: This shows how many mortgage applications make it from approval to closing. A low rate can point to issues in the application process, such as incomplete borrower data or last-minute changes.

Turnaround time: This measures how long a loan stays in processing or underwriting. If one stage takes longer than expected, you can pinpoint where delays are coming from and adjust resource allocation.

Fallout rate: This tracks how many loans don’t close. Common reasons include borrower credit changes, missing paperwork, or shifts in the market. Reviewing these files helps you identify patterns and avoid repeating the same issues.

Monitoring these metrics gives lenders a clearer view of pipeline performance and helps them decide where to focus their efforts.

Why Lenders Need to Carefully Manage Their Mortgage Pipeline

Lenders need to keep a close watch on their mortgage pipeline. Loans move at different speeds, and a missing bank statement, unresolved condition, or extended underwriting can delay an approval.

Interest rate shifts can change the value of loans that haven’t closed yet. For example, Morgan Stanley expects the 30-year fixed mortgage rate to drop to 5.50%–5.75% by mid-2026 and rise again later in the year, affecting margins and revenue.

A mortgage pipeline shows where approvals slow down. When many mortgage brokers submit applications at once, or underwriters face high demand, files sit in processing and delay clients.

Tracking the loan pipeline helps mortgage originators assign work and monitor pull-through rates. It also helps them apply hedging strategies to manage interest rate risk during the mortgage origination process.

Common Challenges in Managing a Mortgage Loan Pipeline

Managing a mortgage pipeline gets difficult when too many files compete for attention. One loan may wait on a missing bank statement, while another gets flagged during underwriting. These gaps delay approvals and extend timelines.

In the mortgage industry, many brokers submit mortgage applications at the same time. Underwriters then face a queue of files, and some remain untouched longer than expected. That delays funding and means lenders have to wait longer to get paid on those loans.

Compliance adds more pressure. Lenders have to follow Fannie Mae guidelines and review every detail in the file. Even a single error in paperwork can pause a loan until it’s corrected.

Loan type also affects how files are handled. A standard W-2 file is quicker to review than a non-qualified mortgage (non-QM) loan with multiple income sources.

When both sit in the same loan pipeline, it’s harder to prioritize which file to review first, which can affect overall performance and profitability.

Best Strategies for Mortgage Pipeline Management

Managing a mortgage pipeline means handling each loan file carefully from intake to closing. You need a consistent method for collecting documents, reviewing loans, and keeping borrowers and real estate agents informed.

Set Clear File Requirements Before Processing

Start with a fixed checklist for every loan. Ask for pay stubs, bank statements, and tax returns before a file enters processing.

Be specific about what underwriting needs. Confirm income calculations, signed disclosures, and credit details upfront. When those pieces are in place early, files don’t get returned for missing information.

Separate Simple and Complex Loans

A W-2 borrower with steady income is easier to review than a file with multiple income sources or self-employment. These loans don’t require the same level of review.

Group similar files together so underwriters can stay focused on one type of review at a time. Many lenders route complex files to experienced reviewers who are used to handling detailed income scenarios.

Balance Workloads Among Underwriters

Keep an eye on how many files each processor and underwriter is handling. If one person has too many loans, reviews take longer, and errors become more likely.

Reassign files when workloads become uneven. During busy periods, some companies bring in contract underwriters to help clear the queue and keep reviews steady.

Review Compliance Before Underwriting

Check key documents early in the process. Verify income, assets, and disclosures before sending a file to underwriting.

Lenders rely on accurate data to meet Fannie Mae and investor requirements. Catching errors early keeps files ready for final approval and avoids late-stage corrections.

How AI Fits Into Your Mortgage Pipeline Process

A mortgage pipeline consists of document review, guideline checks, condition requests, and borrower follow-up. Those tasks take time when loan officers do them manually.

Addy AI helps automate those steps.

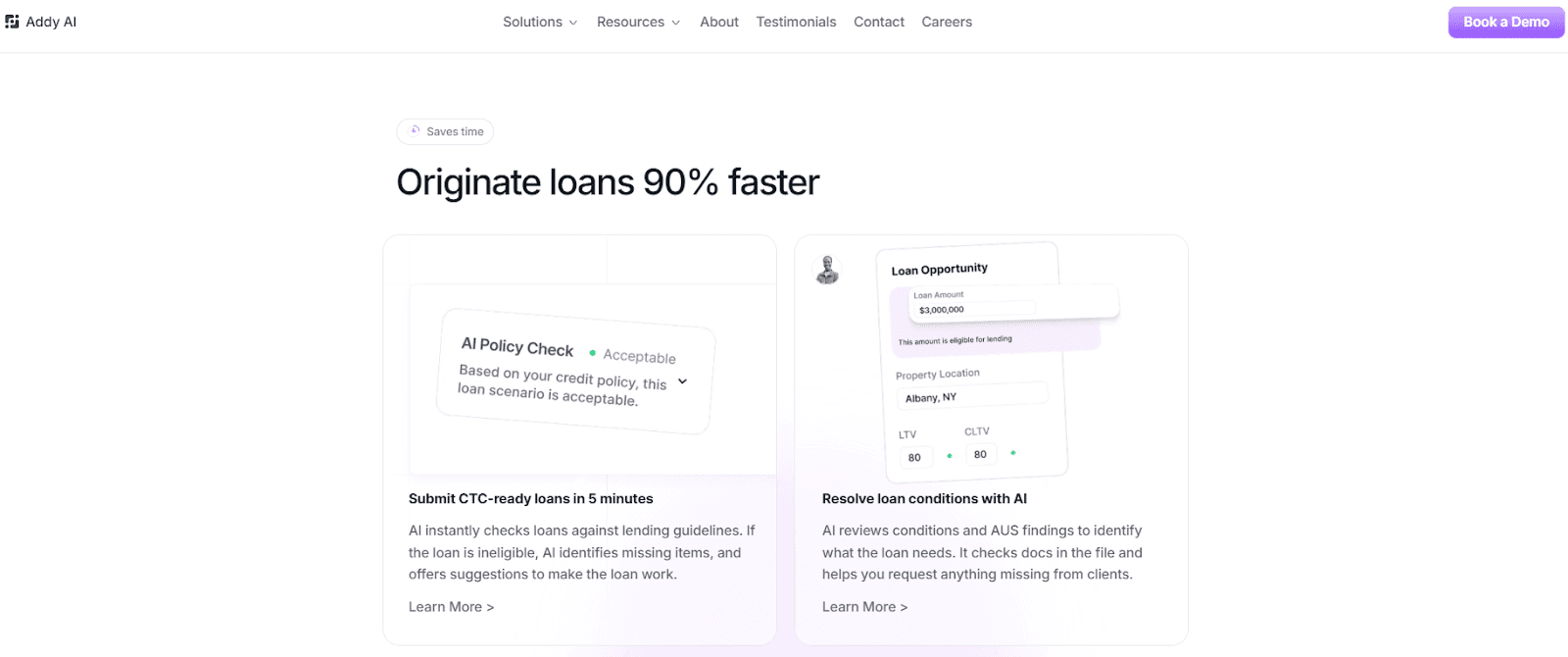

AI-Powered Document Processing

Addy AI reads bank statements, pay stubs, tax forms, emails, and loan documents. It pulls out key details and points out items that need a closer look. If a bank statement shows a large deposit, the system highlights it for review.

It also checks whether the file has the documents needed for the next step. That saves loan officers from scanning every page and figuring out what’s missing on their own.

Automated Follow-Ups and Condition Resolution

Addy AI reviews conditions and automated loan underwriting findings to figure out what a loan still needs. It can request missing documents from borrowers by email or phone, which helps prevent files from waiting too long for a response.

Loan officers can also use it to compare guidelines from Fannie Mae, Freddie Mac, and non-QM lenders. They can ask a question and get an answer based on the guidelines they’ve uploaded.

Integration with LOS, CRM, and Communication Tools

Addy AI connects with your loan origination system (LOS), customer relationship management (CRM) platform, and other business tools. It can sync loan data automatically, so loan officers don’t have to enter the same information again.

They can also use it in Microsoft Teams, Slack, or a browser extension to review files, search guidelines, and request documents while they work.

Keep Your Mortgage Pipeline Organized with Addy AI

Managing a mortgage pipeline means keeping track of documents, conditions, and borrower updates without getting buried in paperwork.

When loan officers don’t have to read every page, send every follow-up, or double-check every guideline, they can keep deals from causing delays.

Addy AI brings that into one workflow. It reviews documents, flags missing items, checks loans against guidelines, and reaches out to borrowers when documents are missing.

It also connects with your LOS and communication tools, so you don’t have to switch between systems. This kind of technology helps lenders handle more files without losing track of important details.

FAQs About Mortgage Pipeline Management

How do mortgage brokers manage a mortgage pipeline?

Mortgage brokers track each loan, follow up on missing documents, and keep borrowers informed. They also decide which files need attention first by setting a clear priority, so approvals don’t get held up.

What is mortgage pipeline hedging?

Mortgage pipeline hedging helps lenders deal with interest rate changes before a loan closes. They often use financial tools like derivatives and mortgage-backed securities to offset potential losses before selling loans.

How can lenders prioritize loans in a mortgage pipeline?

Lenders look at closing dates, document completion, and loan complexity when putting files in order. Loans that are ready for review or close to approval usually go first, while more complex files take longer to work through.

Start closing more loans – Book your demo today

Stay ahead of the competition and discover how AI can accelerate your loan origination process, reduce manual work, and help you close more deals in less time. Book a demo today and start experiencing the future of lending.