Michael Vandi

The mortgage process used to mean paperwork, delays, and constant follow-ups.

Today, the digital mortgage process puts everything online, from application to closing. Borrowers can submit information, upload documents, and sign forms without stepping into an office.

Technological advancements like mortgage AI tools help lenders make more accurate decisions and catch mistakes early.

In this guide, you’ll see how the digital mortgage process unfolds and what makes it faster than the traditional way.

TL;DR

The digital mortgage process completes a loan online from application through closing.

Lenders use software to review income, assets, and credit during the mortgage workflow.

Automation reduces manual data entry so teams can focus on loan decisions.

Consistent execution improves borrower satisfaction and supports long-term success for lenders who invest in better systems.

Addy AI turns documents into loan data and helps lenders keep files ready for underwriting.

What Makes a Mortgage Process “Digital”?

The digital mortgage process is a home loan completed online from start to finish. Borrowers still go through the same steps as a traditional mortgage application process, including credit checks, document submission, underwriting, and closing.

What makes it “digital” is how those steps are done. The application is submitted through a secure portal, and financial documents like pay stubs, bank statements, and tax forms are uploaded as digital files.

During loan processing, artificial intelligence reviews income, employment history, and assets to assist with underwriting decisions. Compared to the traditional process, there’s no need to re-enter the same information into different systems.

What Happens During a Digital Mortgage Process?

Here’s how a fully digital mortgage process works in practice, from the first application to final closing.

1. Online Application and Pre-Qualification

The process starts when a homebuyer fills out the loan application through a secure portal or mobile app. They’ll enter details about income, employment, assets, debts, and the property they’re planning to purchase.

Once submitted, the system reviews that information against basic lending requirements. This gives the applicant an early idea of whether the loan may qualify before a thorough review begins.

2. Credit Checks and Data Verification

After the application is in, the lender pulls the applicant’s credit report through connected digital tools. There’s no need to gather paperwork or send files separately just for this step.

At the same time, the lender can verify income, employment history, and assets through trusted data sources. This gives financial institutions a more complete picture without relying only on uploaded documentation.

3. Document Collection and Uploads

The applicant uploads financial documents through the portal. These usually include pay stubs, W-2s, tax returns, bank statements, and proof of employment.

The system keeps track of what’s been submitted and what’s still needed. This makes it easier for clients to follow along without wondering which documents are still required.

4. Document Processing and Data Extraction

Once the documents are uploaded, AI reads them and extracts key details. It can identify income from pay stubs, account balances from bank statements, and tax information from returns.

That information is then added to the loan system automatically, so loan officers don’t have to enter it line by line. The file is already structured for underwriting, which makes the next review step easier.

5. Automated Underwriting

At this stage, the system reviews the loan file against lending guidelines. It checks credit, income, assets, debts, and other requirements related to the loan.

Machine learning (ML) models help flag potential risks during this review. An underwriter may still look at the file, but much of the initial evaluation is already done.

6. Condition Generation and Resolution

If more information is needed, the system adds conditions to the file. These might include requests for updated bank statements, letters explaining large deposits, or additional proof of income.

Clients receive these requests through the portal, email, or text. As documents are submitted, the loan status updates so everyone involved can see what’s complete and what still needs review.

7. Approval, E-Signing, and Digital Closing

Once everything is reviewed and approved, the final loan documents are sent out for signature. These can be signed electronically without printing or mailing paperwork.

Depending on the setup, the closing may include remote notarization or a mobile notary visit. From start to finish, the entire process can be completed online without going into a physical office.

Where the Fully Digital Mortgage Process Slows Down

Even with digital mortgage solutions in place, many lenders still deal with gaps that slow down the loan processing workflow.

Manual data entry keeps showing up: Loan officers often re-enter the same details into the loan origination system (LOS), customer relationship management (CRM) system, and other digital platforms. This turns what should be a faster workflow into a time-consuming process.

Document collection gets difficult to track: Financial documents come in through different channels, including email and borrower portals. When digital documents aren’t properly linked to the loan file, it’s easy to miss key documentation.

Condition clearing slows everything down: When clients are asked for additional documents, responses don’t always come in right away. Without consistent follow-ups, files remain incomplete longer than expected.

Systems don’t work together: Many financial institutions rely on separate tools that don’t sync. This creates gaps in loan status updates and forces staff to check multiple systems to understand what’s happening.

How Lenders Fix Gaps in the Digital Mortgage Process

Lenders fix gaps in the digital mortgage process by improving how loan files are reviewed and tracked.

First, they cut out repeated data entry. Loan officers send borrower information from the loan application process straight into the LOS and CRM, so the same income, asset, and employment details aren't repeated.

Next, they use automation for routine checks. Software reviews documents against lending guidelines and confirms specific requirements, which keeps loan processing on track without relying solely on manual work.

Then, lenders apply AI and data analytics in underwriting. These tools read financial documents, verify income, and flag risk early in the file.

According to Kellton, advanced ML models have improved loan approval accuracy by about 30%, giving lenders more reliable information during underwriting.

Finally, they connect their systems so that loan data updates automatically. This keeps everyone working with the same information and helps lenders stay competitive in the mortgage industry.

How Addy AI Speeds Up the Digital Mortgage Process

Addy AI improves the digital mortgage process by turning documents into loan data, preparing files before underwriting, and keeping communication active without constant follow-ups.

Turn Documents Into Loan Data Automatically

Addy AI reads financial documents like 1003s, 1040s, W-2s, bank statements, and pay stubs as soon as they’re uploaded. It extracts income, assets, and employment details, then sends that data directly into the LOS.

Documents from email inboxes and internal systems are also matched to the correct loan file. This means loan officers don’t have to open each file and type in numbers manually, which reduces errors and supports faster processing.

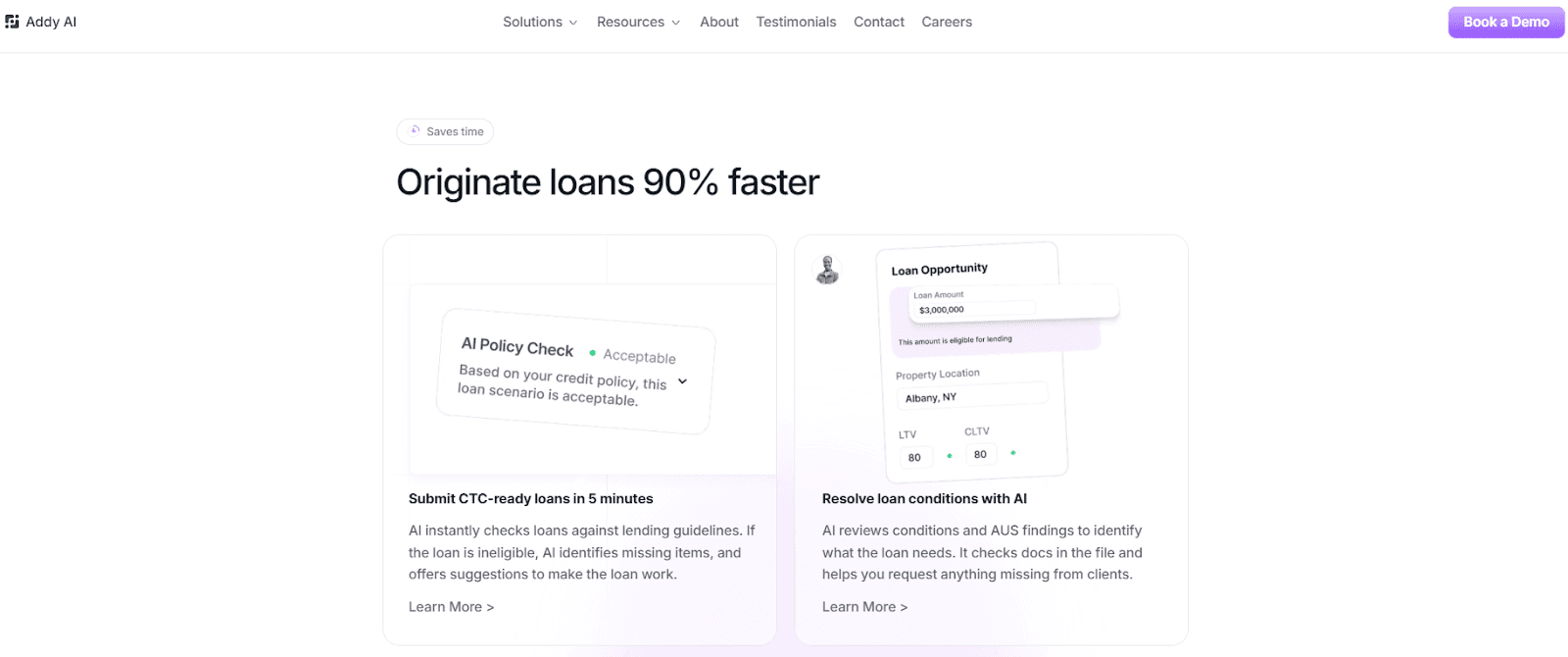

Submit CTC-Ready Loans in Minutes

Addy AI uses a Processing Checklist to review documents and apply product-specific conditions. It shows what’s complete and what’s missing before the file reaches underwriting.

Loan officers can review a prepared file instead of sorting through documents themselves. This helps control costs linked to incomplete or inconsistent files.

Resolve Conditions and Keep Systems Updated

Addy AI reviews automated underwriting system (AUS) findings and identifies outstanding conditions. It sends document requests by email, text, or phone and continues follow-ups until clients submit the required files.

It connects with the LOS, CRM, point of sale (POS), and communication tools. Loan data updates in each system, keep operations consistent, and improve the mortgage experience for buyers and consumers.

Run Your Digital Mortgage Process with Addy AI

Credit checks, document collection, underwriting, and closing still follow the same pattern. What separates lenders in the current digital mortgage landscape is how those steps get done.

Loan officers often type the same income, asset, and employment details in multiple systems. That’s where errors happen, and files get sent back for correction.

In a digital age where consumers expect quick answers, that experience raises concerns for both lenders and buyers.

Addy AI takes over that work. It reads financial documents, extracts income and asset data, and places it into the loan system. It also tracks missing documents and sends follow-ups until the file includes what underwriting needs.

Loan officers can spend their time reviewing loans, answering questions about money, and helping buyers navigate their options.

Online lenders and fintech companies already use mortgage automation software like Addy AI to process more loans without adding staff.

FAQs About the Digital Mortgage Process

What is the digital mortgage process?

The digital mortgage process is a home loan completed online from application to closing. Borrowers submit documents, lenders review them using software, and approvals happen without as much human intervention.

Can you complete a mortgage entirely online?

Yes. You can apply, upload documents, go through underwriting, and sign closing documents online. Many industry leaders offer this setup, so buyers get easier access to loans without visiting an office.

How long does a digital mortgage take?

A digital mortgage can take days instead of weeks, depending on how quickly documents are submitted. Lenders use new technologies to review files faster, which helps shorten approval times.

Is the digital mortgage process safe?

Yes. Lenders use secure portals and encryption to protect your financial information and maintain strong data security. These systems follow strict standards, so your documents stay protected throughout the process.

Start closing more loans – Book your demo today

Stay ahead of the competition and discover how AI can accelerate your loan origination process, reduce manual work, and help you close more deals in less time. Book a demo today and start experiencing the future of lending.