Michael Vandi

Why do so many loans slow down after the application is submitted?

Mortgage operations are still filled with manual steps like reviewing bank statements, checking guidelines, and following up for missing documents. Each delay stretches approval timelines.

In this guide, you’ll see how digital mortgage operations are changing how loans go from application to closing.

TL;DR

Digital mortgage operations use AI and RPA to handle document review, condition checks, and follow-ups.

Manual workflows slow loans when files wait for review, updates, or borrower responses.

AI reads documents, while RPA updates loan data and sends requests automatically.

This approach helps lenders address key challenges and apply a practical digital strategy.

Addy AI uses the right technology to automate these steps and keep loan workflows consistent.

What Are Digital Mortgage Operations?

Digital mortgage operations describe how lenders process loans using systems that take over routine work. The system reads documents, updates loan data, flags missing items, and sends borrower requests as information comes in.

In a traditional mortgage process, a processor opens each file and reviews documents one by one. They update the loan origination system (LOS) and email the borrower if anything is missing. That same routine repeats on every loan and adds time before the file reaches pre-closing.

With digital mortgage operations, the system reads documents as soon as the borrower uploads them. It pulls out key details and flags missing information right away. Loan status updates as conditions are met, and borrowers receive requests without waiting for a follow-up.

Lenders are shifting in this direction since borrowers expect a faster application process, and manual workflows can’t keep up.

Why Borrowers Expect Fully Digital Mortgage Experiences

Borrowers expect a fully digital mortgage experience since most financial services already happen online. That change has raised expectations in the mortgage industry.

Borrowers don’t want to print forms, wait for email replies, or request updates just to understand what’s happening with their loan.

That expectation starts with the application. According to Business Research Insights, 78% of homebuyers prefer online mortgage applications. Once they apply online, the rest of the loan process is expected to follow the same standard.

Borrowers expect immediate updates when documents are missing and want to see progress without contacting a loan officer. When communication is delayed, it becomes harder to track what’s happening with the file.

Mortgage lenders that meet these expectations keep borrowers engaged and more likely to complete the loan process. Those that don’t risk losing deals to lenders that offer a simpler borrower experience.

Core Components of Digital Mortgage Operations

Digital mortgage operations rely on a few core capabilities that automatically handle document review, loan checks, and system updates.

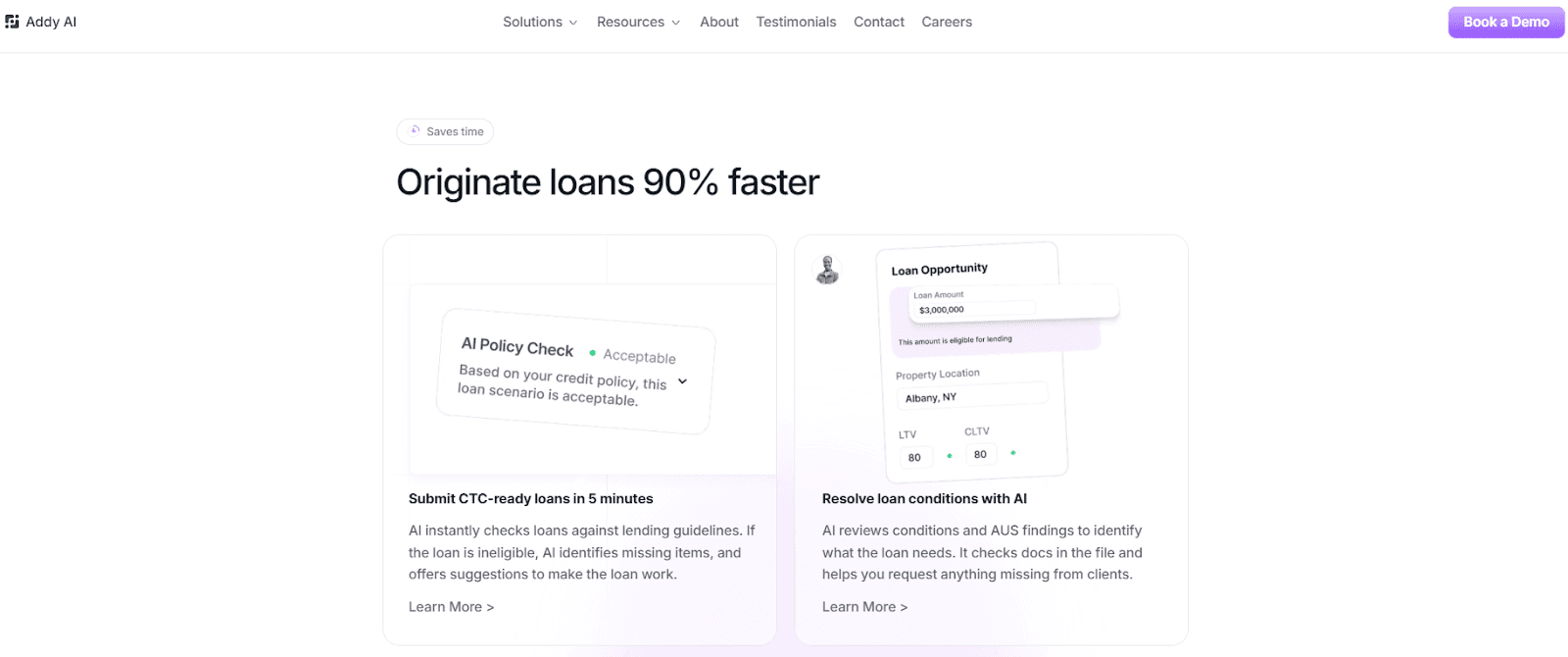

Artificial Intelligence Reviews Documents and Loan Conditions

AI reads borrower documents as soon as they’re uploaded. It uses machine learning to identify income from pay stubs, balances from bank statements, and key details from tax forms.

It also checks those details and flags missing conditions or eligibility issues.

Instead of searching through full documents, loan officers see extracted data points such as income totals, transaction patterns, and flagged anomalies that need attention.

Robotic Process Automation Handles Repetitive Loan Tasks

Robotic process automation (RPA) takes care of steps like entering borrower data into the LOS, updating loan fields, and sending document requests. These are tasks processors repeat on every loan.

When a document is uploaded, RPA logs it, updates the loan record, and triggers the next action if information is incomplete. This removes repeated manual entry and follow-up tracking.

Data Shows Where Loans Slow Down

Digital mortgage solutions use advanced analytics to track how long each step takes in the mortgage process.

Lenders can see where files pause, how long document collection takes, and which conditions hold up pre-closing, without relying on manual notes or email chains.

Connected Systems Keep Loan Information Updated

Mortgage lenders use LOS, customer relationship management (CRM) software, and other digital tools during mortgage lending.

When these systems connect, borrower data, document status, and communication update together. Loan officers can review file progress without checking multiple platforms, which improves the customer experience.

Benefits of Digital Mortgage Operations for Lenders

Digital mortgage operations influence how lenders process loans, manage risk, and handle volume. These changes affect timelines, costs, and borrowers' responses throughout the loan process.

Shorter loan timelines: Automation handles document review, condition checks, and follow-ups as soon as information comes in. Loans that once took weeks can reach clear-to-close (CTC) much sooner.

Stronger compliance and lower risk: Mortgage AI tools flag missing documents, inconsistent data, and incomplete files before underwriting begins. That helps lenders reduce risk and avoid last-minute issues.

Better borrower experience: Borrowers receive updates, document requests, and next steps as changes happen. That keeps borrower engagement high and meets customer expectations during the mortgage process.

Higher loan volume without hiring more staff: Mortgage professionals spend less time reviewing documents or sending reminders. Lenders can process more loans without increasing headcount or costs.

These benefits give lenders a competitive edge in the mortgage business, especially as digital adoption continues to grow.

How to Build a Fully Digital Mortgage Operation

Start with a loan that took longer than expected. Look at what caused the delay: a missing bank statement, a condition waiting for review, or a file that someone had to check twice? That’s where legacy systems tend to slow the mortgage process.

Next, decide what should happen automatically. When a borrower uploads a document, the system should log it, check for missing items, and update the LOS right away. When a condition is met, it should mark it complete and push the file to the next step.

Don’t stop at the application. Many lenders use mortgage technology to collect documents, but the work after that stays manual. A processor still opens every file, enters data into the LOS, and emails the borrower for missing items.

Set it up so the process continues without waiting for manual input. When a borrower uploads a pay stub, the system should recognize it, check for gaps, and update the file.

That’s how digital mortgage operations work in day-to-day lending.

How Addy AI Fits Into Digital Mortgage Operations

Addy AI automates mortgage document processing, underwriting checks, follow-ups, and compliance tasks inside the loan origination process. It gives you faster access to borrower information, guideline answers, and file status.

Turn Loan Files Into Organized Loan Data

When a borrower uploads documents, Addy AI extracts key details from bank statements, pay stubs, tax forms, and other files. It can also summarize emails and borrower communication, then highlight unusual activity such as large transactions that need review.

Loan officers get the important information up front instead of reading every page.

Review Files Before Manual Review Begins

Addy AI identifies missing documents, incomplete information, and outstanding conditions before file review starts. It also runs product-specific conditions and builds a processing checklist to prepare the loan.

Loan officers can compare guidelines from Fannie Mae, Freddie Mac, and non-qualified mortgage (non-QM) lenders in natural language, which helps with lender selection and meeting customer needs.

Follow Up on Missing Documents and Keep Systems Updated

When documents are missing, Addy AI contacts borrowers by email or phone and continues follow-ups until the file is complete. It can also draft personalized messages, which helps maintain a consistent customer experience.

At the same time, Addy AI integrates with the LOS and CRM platform. You don’t have to switch between systems or log updates manually.

Automate Digital Mortgage Operations With Addy AI

Digital mortgage operations solve coordination issues between document review, communication, and loan updates. Delays often happen when a file is ready for the next step, but no one has flagged it, or when real estate professionals ask for updates that haven’t been recorded.

A connected workflow keeps loan data, document status, and communication in sync as the file progresses. When a document is uploaded or a condition is met, that update reflects right away. This keeps transactions organized from application through post-closing.

It also creates a record lenders can use for valuable insights. For example, past loan data can highlight borrowers who may qualify for refinance or need follow-up at a specific time.

This is where digital transformation delivers results. It connects every step, so updates don’t get missed, and files don’t stall.

Addy AI applies this inside your workflow. It extracts data from documents, flags missing items, runs condition checks, and automates follow-ups while syncing with your LOS and CRM.

Book a demo with Addy AI to see how your loan process can run with fewer interruptions.

FAQs About Digital Mortgage Operations

Can digital mortgage operations replace loan processors?

No. They take over repetitive steps like checking documents and sending follow-ups, so loan processors can focus on reviewing loans and making decisions. That helps lenders focus on work that directly supports business goals.

How do digital mortgage operations improve loan timelines?

Digital mortgage operations review documents, track conditions, and send borrower updates as soon as information comes in. Files don’t sit waiting between steps, which helps lenders stay ahead of delays that usually slow down the process.

Do digital mortgage operations help after closing?

Yes. Lenders can use loan data to follow up with past borrowers, spot refinance opportunities, and offer home equity loans when the timing makes sense. This keeps them active with clients instead of starting from zero with every new loan.

Start closing more loans – Book your demo today

Stay ahead of the competition and discover how AI can accelerate your loan origination process, reduce manual work, and help you close more deals in less time. Book a demo today and start experiencing the future of lending.