Michael Vandi

Closing a mortgage loan can still take over a month, and that delay often costs lenders valuable opportunities.

According to AmeriSave, the mortgage process takes 30 to 45 days from application to closing.

As borrowers expect faster approvals and clearer communication, traditional processes are starting to fall behind. Lenders are turning to automated loan decisioning to handle approvals and keep up with borrower demand.

In this guide, you’ll see how it works and what makes it effective at delivering faster loan approvals.

TL;DR

Automated loan decisioning reviews loan applications using data, rules, and models to return credit decisions without manual review.

It checks borrower data, documents, and lending guidelines to flag missing items and assess risk in real time.

Lenders use it to speed up application reviews and keep decisions consistent from one file to the next.

It helps identify qualified borrowers and detect risks using more detailed financial data.

Addy AI uses automated loan decisioning to review loan files, flag issues, and prepare CTC-ready submissions faster.

What Is Automated Loan Decisioning?

Automated loan decisioning uses artificial intelligence (AI) and machine learning (ML) to review a loan application and make credit decisions without manual underwriting.

A system takes in data like bank statements, credit reports, and financial statements, then checks it against lending policies.

It pulls key financial data from credit bureaus and other sources, runs credit checks, and evaluates risk in real time. It can also use alternative data, such as utility payment history, to get a fuller view of the borrower.

How Automated Loan Decisioning Works

Automated loan decisioning follows a set sequence from application to funding. Here’s what happens during the loan approval process.

Digital Application Intake

Borrowers complete an online loan application with details like income, employment history, and loan amount. The application form requires all key fields before submission, so lenders receive complete borrower information upfront.

Loan officers don’t have to go back and request missing basics like income or contact details.

Real-Time Data Aggregation and Validation

An automated loan decisioning platform collects borrower data from credit bureaus, bank accounts, and identity verification services. It compares stated income with bank deposits and checks personal details against official records.

The platform flags mismatches right away, such as income that doesn’t match account activity.

AI-Powered Risk Modeling and Eligibility Checks

ML models evaluate the borrower’s financial profile using scoring models. They review traditional credit scores along with income patterns, payment history, and other financial signals.

Lenders use this information to assess risk and avoid approving high-risk borrowers.

Intelligent Document Processing and Verification

Document processing software reads uploaded files like pay stubs, tax returns, and bank statements. It extracts key details such as income, balances, and transaction history, then compares them with the loan application.

Loan officers don’t need to scan every document line by line to verify the same information.

Instant Decisioning with Conditional Logic

A decision engine applies lending policies to verified borrower data and returns a result. It can approve the loan, decline it, or list conditions such as missing documents or unclear financial details.

The decision engine flags applications that fall outside the rules for manual review.

Digital Closing and Automated Fund Disbursement

Borrowers sign loan documents electronically after approval. Loan origination software finalizes the file and sends it to funding systems.

Lenders release funds sooner and keep the loan approval process on track without unnecessary delays.

How Lending Systems Evaluate Applications

Automated loan decisioning relies on several technologies that support different stages in the loan application process, from intake to final decision.

AI reviews collected data like credit reports and income details, then applies lending policies to guide automated loan underwriting. This replaces outdated manual decision-making that slows approvals.

ML learns from past lending decisions and improves risk assessment over time. It helps identify creditworthy applicants and strengthens fraud detection by spotting inconsistencies in financial data.

Robotic process automation (RPA) handles repetitive tasks like data entry and moving information between existing systems, so loan data doesn’t need to be entered multiple times.

Generative AI helps interpret unstructured data like bank statements, financial statements, and borrower emails by highlighting key financial details that need attention during review.

Together, these technologies support automated mortgage processing and improve loan approval rates while keeping decisions consistent throughout the loan evaluation process.

Want to see how this works inside your lending workflow? Book a demo with Addy AI today!

Why Lenders Are Replacing Manual Decisioning Models

Lenders are moving away from manual decisioning models mainly due to time delays and inconsistent outcomes.

A loan officer often reviews documents, requests missing details, and waits for responses before making a decision, which stretches processing time.

Manual reviews also vary from one person to another. Different interpretations can lead to inconsistent data and make risk management harder to maintain.

As application volume increases, financial institutions need more staff to keep up. That drives up operational costs and strains operational resources.

Manual decisioning also relies on a limited set of data. Without using multiple sources, lenders can miss creditworthy applicants or overlook signals that should trigger fraud checks.

Benefits of Using Automated Loan Decisioning

Automated loan decisioning changes how lenders evaluate risk, reach more borrowers, and stay within regulatory guidelines. It gives the lending business a more reliable view of each application by working with consistent data.

Lenders can spot qualified borrowers more accurately when they look at real income activity and payment behavior. That helps improve the automated approval rate without taking on unnecessary risk.

It also opens new growth opportunities. Credit unions and other lenders can work with applicants who don’t have strong credit histories but still show steady financial behavior. This helps them serve more applicants without lowering standards.

On the compliance side, automated decisioning applies the same rules to every application. Lenders no longer rely on scattered checks in multiple systems, which lowers the chances of missing mortgage fraud red flags.

How Addy AI Applies Automated Decisioning to Loan Files

Addy AI brings auto-decisioning into the loan review process without increasing manual work. Loan officers can review files, assess guideline compliance, and move applications forward without waiting for repeated follow-ups.

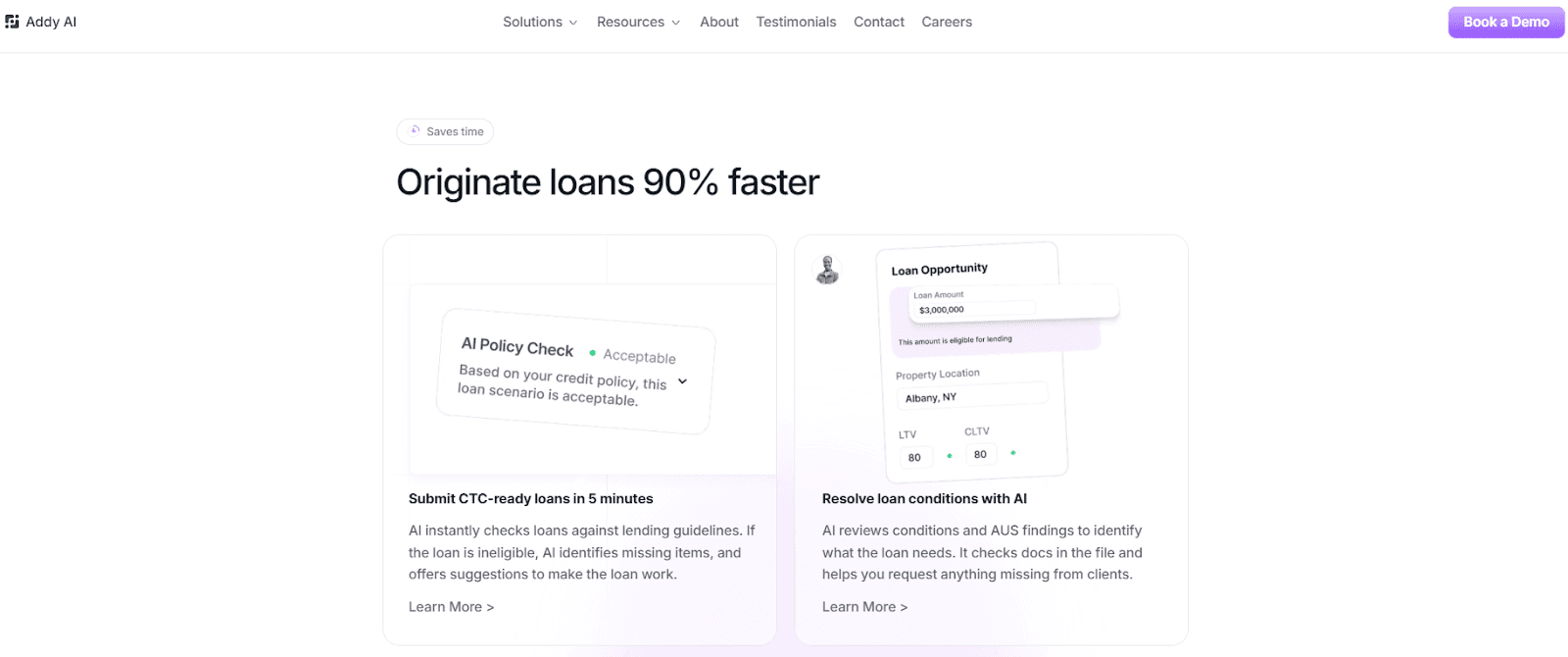

Instant Loan Analysis and Guideline Comparison

Addy AI reviews a loan file and checks it against lender guidelines in minutes. If a file doesn’t meet requirements, Addy AI points out missing documents or mismatched details and suggests what needs to be updated.

Loan officers can also compare guidelines from Fannie Mae, Freddie Mac, and non-qualified mortgage (non-QM) lenders without opening separate documents. This reduces human error and helps structure loans with fewer revisions.

Condition Reviews and Follow-Ups

Addy AI reviews automated underwriting system (AUS) findings and loan conditions to identify what the file still needs. It checks documents already uploaded and sends requests to borrowers by email or phone for anything missing.

This keeps applications active and helps maintain customer relationships without constant manual outreach.

Document Insights and System Integration

Addy AI reads bank statements, pay stubs, and borrower emails, then highlights details like large transactions or income gaps.

It connects with your loan origination system (LOS) and customer relationship management (CRM) platform, so loan data updates without re-entry.

This cuts down errors and helps shorten funding times.

Why Automated Loan Decisioning Is No Longer Optional

Borrowers don’t want to wait for days to hear back after submitting a loan application. They expect quick answers and regular updates, not silence while someone reviews documents. When that doesn’t happen, they move on to another lender.

At the same time, other lenders already use automated decisioning to review applications and respond much faster. If your process takes longer, you’re losing deals to competitors who reply first.

Lending decisions now rely on more detailed financial data, not just basic credit information. Manual reviews can’t keep up with the volume and depth of data that lenders use today.

Automated loan decisioning is already part of how many financial institutions review applications and compete in the market. Without it, it becomes harder to keep up with borrower expectations and ongoing digital transformation.

Turn Loan Files Into CTC-Ready Submissions With Addy AI

Lenders need a faster way to move loan files from review to closing without getting stuck on missing details or guideline checks.

Addy AI reviews loan files, checks them against lender guidelines, and shows what’s missing before final approval.

It also reviews conditions and AUS findings, then points out what the loan still needs. Addy AI analyzes bank statements, emails, and loan documents to highlight items like large transactions that need a closer look.

Loan officers can compare guidelines from Fannie Mae, Freddie Mac, and non-qualified mortgage (non-QM) lenders, request missing documents from borrowers, and sync loan data with their LOS.

This shortens review time and helps turn each file into a CTC-ready loan.

FAQs About Automated Loan Decisioning

How does artificial intelligence improve automated loan decisioning?

Artificial intelligence reviews borrower data, loan documents, and lender guidelines at the same time, so lenders don’t have to check everything by hand.

It flags missing information, spots risks like unusual transactions, and keeps decisions consistent from one application to the next.

How fast can automated loan decisioning process applications?

Automated loan decisioning can review and return a decision in minutes once all required information is in the file. That’s much faster than manual reviews, which can take hours or even days.

Does automated loan decisioning replace underwriters?

Automated loan decisioning doesn’t replace underwriters. It takes care of initial checks and routine reviews, while underwriters focus on complex files, exceptions, and final decisions.

Start closing more loans – Book your demo today

Stay ahead of the competition and discover how AI can accelerate your loan origination process, reduce manual work, and help you close more deals in less time. Book a demo today and start experiencing the future of lending.