Michael Vandi

Why does a file that looks complete still get sent back for more conditions?

It’s usually not a major red flag. It’s a mismatched detail, a guideline that needs another check, or a key piece of information buried in the documents.

That’s where a lot of time gets lost in mortgage lending.

AI-powered mortgage solutions give lenders a more effective way to catch these issues earlier and keep loans progressing.

In this guide, you’ll see how AI mortgage technology is used to improve how loans move from application to approval.

TL;DR

AI mortgage technology helps lenders review documents, improve data quality, and move loans from application to approval faster.

Intelligent document processing extracts borrower data from files like bank statements, tax returns, and loan applications.

Automated underwriting, predictive analytics, and AI valuation help assess eligibility, risk, and property accuracy.

AI chatbots and workflow automation handle borrower communication, document requests, and loan status updates.

Addy AI connects these technologies to process loans faster, reduce manual work, and improve loan throughput.

What Is AI Mortgage Technology?

AI mortgage technology is software used in mortgage lending to review documents, analyze borrower data, and assist with decisions during the loan process.

It helps lenders:

Extract data from bank statements, pay stubs, and tax returns

Check loan files against lending guidelines and regulatory compliance rules

Identify missing documents or inconsistent details

Support credit and risk assessment using borrower data

Loan officers and underwriters still make the final decisions. AI is used to handle repetitive tasks so they can focus on reviewing loans and improving the borrower experience.

6 Types of AI Mortgage Technology Used in Lending

Lenders use different types of AI mortgage technology at key points in the loan process. Here are the main types of AI mortgage technology used in lending today.

1. Intelligent Document Processing for Mortgage Files

Intelligent document processing (IDP) reads loan documents and turns them into usable data.

It uses machine learning, optical character recognition (OCR), and natural language processing (NLP) to understand files like 1003s, W-2s, bank statements, and tax returns.

In the mortgage underwriting process, IDP pulls out key details like income, assets, and employment history.

It also checks those details against each other, so it can catch missing pages or numbers that don’t match before an underwriter opens the file.

When a borrower uploads documents, IDP sends the extracted data into the loan origination system (LOS). Loan officers don’t need to type in the same information again or search through files to find it.

That means underwriters start with a file that already has the right data in place, so they can focus on reviewing the loan and making a decision.

2. Automated Underwriting for Loan Approval

Automated underwriting checks if a loan qualifies using borrower data and lender rules. It reviews income, credit, assets, and debt-to-income ratio using automated underwriting system (AUS) findings and program guidelines used in the mortgage industry.

Here’s what it checks before an underwriter reviews the file:

Does the borrower meet income and debt-to-income requirements?

Does the loan qualify for approval, or does it need conditions?

What exact conditions need to be cleared before approval?

Does the file meet regulatory compliance rules required by financial institutions?

In AI mortgage underwriting, underwriters open a file and immediately see what needs attention. If income from bank statements falls short, the system flags it. If a condition requires updated documents, the processor knows what to request right away.

That shortens processing time and helps mortgage teams reach faster loan approvals without reviewing the same file again.

3. AI Chatbots and Virtual Assistants for Borrower Retention

Basic chatbots answer simple questions like loan status or required documents. They follow set replies, so they stop being useful once a borrower asks something more specific.

AI virtual assistants use AI algorithms to understand what the borrower is asking and respond with relevant details. They can explain why a document is needed, what condition is still open, or what affects the loan approval.

During the loan process, they can:

Send reminders when documents like bank statements or pay stubs haven’t been submitted

Follow up until the borrower uploads what the underwriter requested

Answer questions about loan status, conditions, or interest rates

Track borrower responses so loan officers don’t ask for the same document twice

In AI mortgage lending, this cuts down the time loan officers spend calling or emailing borrowers. They don’t have to check who replied or who still owes documents.

Borrowers get answers right away, which improves the customer experience and keeps the file moving without long gaps in communication.

4. AI Property Valuation for Appraisal Review

AI property valuation reviews appraisal reports, comparable sales, and property photos to check if the value in the report makes sense.

It compares what the appraiser wrote with actual data from the property and nearby sales, so lenders aren’t relying on one opinion alone.

In practice, it points out specific issues that can affect a loan. For example, an appraiser might add value for a renovation, and the system checks the photos to confirm it exists.

A report might list a home in “excellent condition,” but the images show visible damage, which gets flagged for review. It also catches missing photos or incomplete sections before the file reaches underwriting.

These issues show up more often than expected. According to Restb.ai, 33.6% of appraisals show high risk, and 73.9% show medium risk of incorrect or missing adjustments. That puts lenders at risk of buying back loans based on inaccurate property values.

By catching these problems early, lenders base decisions on more reliable data and review appraisals with greater confidence.

5. Predictive Analytics for Risk Assessment

Predictive analytics uses borrower behavior, payment history, and property data to estimate what may happen during the loan lifecycle.

It reviews large amounts of data to spot patterns linked to default rates, refinance timing, and long-term borrower activity.

A borrower who’s been paying on time for years and has built equity may qualify for a refinance when interest rates drop. At the same time, late payments or sudden changes in payment patterns can signal higher risk much earlier.

Lenders use these signals to decide when to reach out. They can offer a refinance at the right time or contact borrowers before payment issues grow.

This gives lenders reliable data for decision-making, helps mitigate risk, and increases repeat business without relying only on manual review.

6. AI-Powered Workflow Automation for the Mortgage Process

AI-powered workflow automation connects steps in the loan process so tasks trigger based on status, not reminders. It uses AI-driven automation to move a file forward as soon as a requirement is completed, without waiting for someone to check it.

In a real loan file, this looks like:

The file is sent to underwriting once all required conditions are complete

Closing documents are sent for e-signature after approval

Loan status updates automatically at each stage

The next team member is notified when the file is ready for review

Loan officers and processors don’t need to check file status or ask who’s responsible next. The file progresses based on completed requirements.

This leads to higher throughput and cost reduction, since teams spend less time on status checks and follow-ups.

How Addy AI Combines AI Mortgage Technologies

Addy AI brings document review, loan checks, borrower outreach, and LOS sync into one platform. Mortgage brokers and lenders can prepare files, review conditions, and collect required documents without switching systems.

Addy AI Combines Document AI, Agents, Checklists, and LOS Sync

Addy AI reads borrower documents like 1003s, 1040s, W-2s, bank statements, and tax returns, then pulls key data from each file. It also pulls documents from borrower inboxes and the LOS, sorts them, and links them to the correct loan.

Loan officers don’t search emails, upload files one by one, or enter the same data twice. The same data appears in the LOS, customer relationship management (CRM), point-of-sale (POS), and tools like Gmail, Outlook, Slack, and Microsoft Teams.

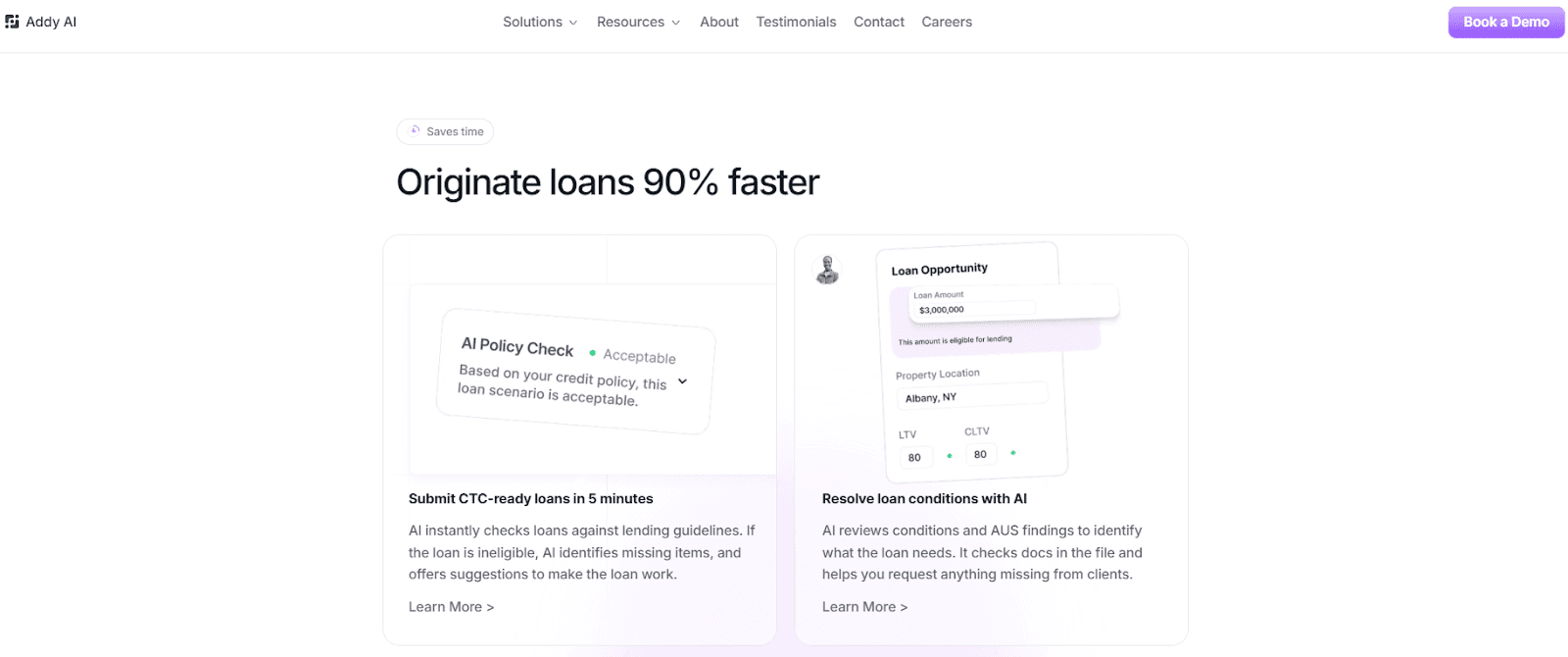

Submit CTC-Ready Loans in 5 Minutes

The Processing Checklist reviews the loan file against lender guidelines and AUS findings. It marks completed conditions and flags missing ones.

When a loan doesn’t qualify, the checklist shows what the file needs. Loan officers use that information to assess creditworthiness using the actual documents in the file.

AI Agents That Request Documents and Resolve Conditions

AI agents contact borrowers by email, text, or phone to request the exact documents tied to open conditions. They follow up until the borrower submits what’s required.

Lenders can use pre-built agents or create their own using internal guidelines and rate sheets. This cuts manual intervention and saves time spent on repeated follow-ups.

Loan officers can also use Addy AI’s browser extension inside their LOS, POS, or CRM. They can review files, check guidelines, compare loan scenarios, and send requests without leaving the screen.

Secure AI Mortgage Technology for Enterprise Lenders

Addy AI meets SOC 2 Type 1 standards and protects borrower data during loan processing. Lenders control who can access files and how data is used.

Teams that work with large datasets and strict compliance rules keep human oversight in place while using AI to review and prepare loan files.

Move Loan Files From Intake to Approval Faster With Addy AI

Addy AI helps lenders originate loans up to 90% faster by removing the steps that usually slow approvals. It uses AI technology to bring together data from documents, emails, and systems, so loan officers don’t have to piece everything together manually.

One example comes from Sphinx Capital, a nationwide lender. Before using Addy AI, their team spent 10 to 60 minutes building a single deal summary.

With Addy AI, those summaries are generated in about a minute using data from vast datasets across documents, emails, and their LOS. That change allowed them to handle more deals without increasing workload.

Borrowers get faster responses and clearer communication. Lenders can take on more borrowers while keeping operations consistent, which gives them a competitive edge.

See how quickly loans can move from application to approval. Book a demo with Addy AI today!

FAQs About AI Mortgage Technology

Can AI mortgage technology help with non-QM loans?

Yes, it can. AI reviews bank statements, tax returns, and income records that don’t follow standard guidelines, which is common in non-qualified mortgage (non-QM) loans.

It helps lenders catch missing documents or mismatched income details early without compromising speed.

Does AI replace loan officers?

No, it doesn’t. AI takes care of tasks like checking documents, tracking conditions, and following up with borrowers, but loan officers still review the file and make the final call.

What should lenders look for in AI mortgage software?

Look for software that can read borrower documents, match them to loan requirements, and show exactly what’s missing or complete.

Mortgage AI tools that create transparent processes help lenders track loan progress and confirm document accuracy at every stage.

Start closing more loans – Book your demo today

Stay ahead of the competition and discover how AI can accelerate your loan origination process, reduce manual work, and help you close more deals in less time. Book a demo today and start experiencing the future of lending.